As I write this blog on the 8th January, I’ve just finished reading lots of positive emails from mainstream lenders confirming interest reductions on their fixed mortgage rates in 2024.

That’s certainly welcome news after the uncertainty of 2023 when rates were all over the place.

It created a lot of stress for clients coming out of a mortgage deal with a much lower rate.

Why Have Mortgage Rates Started to Fall?

I think there are two main reasons driving mortgage rate cuts:

- There has been a reduction in swap rates. These are the rates that lenders “swap” interest loans between each another and affects mortgage rates we all pay.

- Many lenders are pre-empting these reductions and competing on price, which is great news for borrowers.

For example, one major high street bank has reduced the interest on their five year fixed rate mortgage deals, with a 60% loan to value, to below 4% which is an important level.

Of course, rates are always subject to change, but this may prompt other mainstream mortgage lenders to follow suit.

Will Mortgage Rates Continue to Fall in 2024?

Like me, your first reaction to this news is probably how long is this going to last?

No one really knows, but many industry experts believe interest rates have peaked and will keep falling in 2024 as inflation pressures reduce towards the end of the year.

Mortgage rate predictions are based on several variables such as swap rates, gilt rates, the Bank of England base rate, inflation, and GDP (Growth Domestic Product).

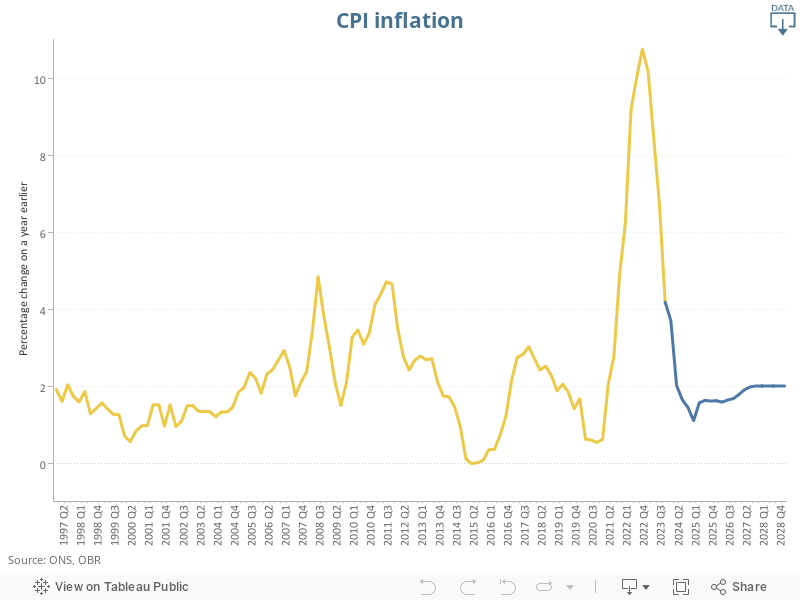

Inflation

The good news is that inflation has more than halved from a high of 10.1% at the beginning of 2023 to 3.9% today.

However, it’s still almost double the Government’s target of 2% so we still have some way to go.

Forecasts by the Office for Budget Responsibility show inflation falling rapidly between 2024 and 2026, reaching the 2% target by the end of 2026.

Base Rate

More reassuring news is that the Monetary Policy Committee have left the Bank of England Base Bate unchanged for the last 3 consecutive meetings.

This has given the mortgage and property markets confidence that things may settle down this year.

In fact, if inflation continues to fall, they will be under pressure for an interest rate cut.

House Prices

The housing markets seem to have ended on a high in 2023 which is another promising sign.

According to Halifax House Price Index, the average UK house price rose for the 3rd consecutive month in December to £287,105.

This shows that despite a challenging 2023, the property market is resilient and has got off to a positive start in 2024.

What To Watch Out For

Despite lots of good news, there are some things to watch out for this year.

GDP shrunk in October and if this continues there could be a recession on the horizon. The Bank of England confirmed there is a 50/50 chance of a recession this year and expects zero growth for 2024.

There is also a potential general election this year that is likely to influence economic stability and interest rates.

Are You Prepared?

There are lots of variables that could affect the mortgage markets in 2024. The important thing is to take advantage of the current trend and ensure you’re prepared for any scenario.

Now is a great time to review your mortgage affordability and borrowing options.

So, whether you are a first time buyer looking to get on the property ladder, a homeowner thinking of moving, or an existing borrower with a fixed rate deal ending this year — get in touch to book a free consultation.

ABOUT THE AUTHOR